This notebook is part of a GitHub repository: https://github.com/pessini/insurance-claim-prediction/

This notebook is part of a GitHub repository: https://github.com/pessini/insurance-claim-prediction/

MIT Licensed

Author: Leandro Pessini

This notebook is part of a GitHub repository: https://github.com/pessini/insurance-claim-prediction/

MIT Licensed

Author: Leandro Pessini

Porto Seguro’s Safe Driver Prediction - Kaggle

¶

![]()

Porto Seguro is one of the largest insurance companies in Brazil specialized in car and home insurance. Located in São Paulo, Porto Seguro has been one of the leading insurers in Brazil since its foundation in 1945.

A key challenge faced by all major insurers is, when it comes to car insurance, how to address fairness towards good drivers and try not to penalize those who have a good driving history on account of a few bad drivers. Inaccuracies in car insurance claim predictions usually raise its cost for good drivers and reduce the price for bad ones.

Porto Seguro has been applying Machine Learning for more than 20 years and intends to make car insurance more accessible to everyone.

![]()

Kaggle is an online community of data scientists and allows users to find and publish data sets, explore and build ML models, and enter competitions to solve data science challenges.

In this competition, the challenge is to build a model that predicts the probability that a car insurance policyholder will file a claim next year.

In the train and test data:

ind, reg, car, calc). bin to indicate binary features and cat to indicate categorical features.-1 indicate that the feature was missing from the observation. target columns signifies whether or not a claim was filed for that policy holder. import numpy as np

import pandas as pd

import matplotlib

import matplotlib.pyplot as plt

import matplotlib.pylab as pylab

import seaborn as sns

import random

import json

from pathlib import Path

%matplotlib inline

matplotlib.style.use("ggplot")

# Preprocessing

import sklearn

from sklearn.preprocessing import StandardScaler

from sklearn.preprocessing import MinMaxScaler

from sklearn.model_selection import KFold

from sklearn.model_selection import StratifiedKFold

from sklearn.model_selection import train_test_split

# Models

import lightgbm as lgb

from lightgbm import LGBMClassifier

import xgboost as xgb

from xgboost import XGBClassifier

import joblib

from numpy import savetxt

from numpy import loadtxt

# Evaluation

from sklearn.metrics import roc_auc_score

from sklearn.metrics import auc

from sklearn.metrics import roc_curve

from numpy import argmax

# Hyperparameter optimization

from sklearn.model_selection import RandomizedSearchCV

import time

import warnings

warnings.simplefilter('ignore', FutureWarning)

from platform import python_version

print('Python version:', python_version())

Python version: 3.8.5

# !pip install -q -U watermark

%reload_ext watermark

%watermark -a "Leandro Pessini" --iversions

Author: Leandro Pessini seaborn : 0.11.1 joblib : 1.0.1 sklearn : 0.23.2 numpy : 1.19.2 json : 2.0.9 xgboost : 1.4.1 matplotlib: 3.3.2 lightgbm : 3.1.1 pandas : 1.1.3

# Kaggle

#path = "../input/porto-seguro-safe-driver-prediction/"

# Local

path = "./data/"

%%time

train_df = pd.read_csv(path + "train.csv").set_index('id')

test_df = pd.read_csv(path + "test.csv").set_index('id')

CPU times: user 9.78 s, sys: 2.27 s, total: 12.1 s Wall time: 14.3 s

As per competition description, there are a few calculated features. In one of the discussions on Kaggle, it was highlighted that some kind of transformation was applied in order to generate these features. I will drop them and apply the transformations using my best judgment.

train_df = train_df.drop(train_df.filter(regex='_calc').columns, axis=1)

test_df = test_df.drop(test_df.filter(regex='_calc').columns, axis=1)

print('Train Dataset - Number of rows are',train_df.shape[0], 'and number of columns are ',train_df.shape[1])

print('Test Dataset - Number of rows are',test_df.shape[0], 'and number of columns are ',test_df.shape[1])

Train Dataset - Number of rows are 595212 and number of columns are 38 Test Dataset - Number of rows are 892816 and number of columns are 37

target variable 1 means that a claim was filed and 0 that it was not claimed.

y = train_df.target

fig = plt.figure(figsize=(7, 5))

ax = sns.countplot(y,label="Count")

total_size = len(train_df)

# Display the target value ratio at the top of the bar

for patch in ax.patches:

height = patch.get_height()

width = patch.get_width()

left_coord = patch.get_x()

percent = height/total_size*100

ax.text(x=left_coord + width/2.0,

y=height + 3000,

s='{:1.1f}%'.format(percent),

ha='center')

ax.set_title('Target Distribution');

plt.savefig('./plots/target_distribution.png', dpi=fig.dpi)

The target feature has a severe imbalance distribution showing that only 3.6% filled a claim and 96.4% did not.

This will be handle by the algorithm on a hyperparameter is_unbalance = True.

vars_with_missing = []

for f in train_df.columns:

missings = train_df[train_df[f] == -1][f].count()

if missings > 0:

vars_with_missing.append(f)

missings_perc = missings/train_df.shape[0]

print('Variable {} has {} records ({:.2%}) with missing values'.format(f, missings, missings_perc))

print('\nIn total, there are {} variables with missing values'.format(len(vars_with_missing)))

Variable ps_ind_02_cat has 216 records (0.04%) with missing values Variable ps_ind_04_cat has 83 records (0.01%) with missing values Variable ps_ind_05_cat has 5809 records (0.98%) with missing values Variable ps_reg_03 has 107772 records (18.11%) with missing values Variable ps_car_01_cat has 107 records (0.02%) with missing values Variable ps_car_02_cat has 5 records (0.00%) with missing values Variable ps_car_03_cat has 411231 records (69.09%) with missing values Variable ps_car_05_cat has 266551 records (44.78%) with missing values Variable ps_car_07_cat has 11489 records (1.93%) with missing values Variable ps_car_09_cat has 569 records (0.10%) with missing values Variable ps_car_11 has 5 records (0.00%) with missing values Variable ps_car_12 has 1 records (0.00%) with missing values Variable ps_car_14 has 42620 records (7.16%) with missing values In total, there are 13 variables with missing values

Only ps_car_03_cat and ps_car_05_cat have a large number (~ >= 50%) of missing values.

To make data management easier, a meta-info about the variables is added to the DataFrame. It will help handling those variables later on the analysis, data viz and modeling.

We do not have information on which features are ordinal or not so a meta-info numerical will be added in order to apply Normalization later.

data = []

for f in train_df.columns:

if 'bin' in f or f == 'target':

level = 'binary'

elif 'cat' in f:

level = 'categorical'

elif train_df[f].dtype == float:

level = 'numerical'

elif train_df[f].dtype == int:

level = 'numerical'

# Defining the data type

dtype = train_df[f].dtype

# Creating a Dict that contains all the metadata for the variable

f_dict = {

'varname': f,

'level': level,

'dtype': dtype

}

data.append(f_dict)

meta = pd.DataFrame(data, columns=['varname', 'level', 'dtype'])

meta.set_index('varname', inplace=True)

# Example to extract all categorical variables that are not dropped

meta[(meta.level == 'categorical')].index

Index(['ps_ind_02_cat', 'ps_ind_04_cat', 'ps_ind_05_cat', 'ps_car_01_cat',

'ps_car_02_cat', 'ps_car_03_cat', 'ps_car_04_cat', 'ps_car_05_cat',

'ps_car_06_cat', 'ps_car_07_cat', 'ps_car_08_cat', 'ps_car_09_cat',

'ps_car_10_cat', 'ps_car_11_cat'],

dtype='object', name='varname')

pd.DataFrame({'count' : meta.groupby(['level'])['level'].size()}).reset_index()

| level | count | |

|---|---|---|

| 0 | binary | 12 |

| 1 | categorical | 14 |

| 2 | numerical | 12 |

numerical_features = meta[(meta.level == 'numerical')].index

fig = plt.figure(figsize=(12, 10))

cont_corr = train_df[numerical_features].corr() # Correlation between continuous features

sns.heatmap(cont_corr, annot=True, cmap='OrRd'); # Plot heatmap

plt.savefig('./plots/heatmap.png', dpi=fig.dpi)

There are a strong correlations between the variables:

Heatmap showed low number of correlated variables, we'll look at three of highly correlated variables separately.

# Convert -1 from training data copy to np.NaN

train_copy = train_df.copy().replace(-1, np.NaN)

train_copy = train_copy.dropna()

s = train_copy.sample(frac=0.2)

NOTE: sampling was applied to speed up the process.

sns.lmplot(x='ps_car_12', y='ps_car_13', data=s, hue='target', palette='Set1', scatter_kws={'alpha':0.3})

plt.savefig('./plots/ps_car_12xps_car_13.png', dpi=fig.dpi)

plt.show()

sns.lmplot(x='ps_reg_01', y='ps_reg_03', data=s, hue='target', palette='Set1', scatter_kws={'alpha':0.3})

plt.savefig('./plots/ps_reg_01xps_reg_03.png', dpi=fig.dpi)

plt.show()

sns.lmplot(x='ps_reg_02', y='ps_reg_03', data=s, hue='target', palette='Set1', scatter_kws={'alpha':0.3})

plt.savefig('./plots/ps_reg_02xps_reg_03.png', dpi=fig.dpi)

plt.show()

As the number of correlated variables is rather low, dimensionality reduction will not be applied and the model will do the heavy-lifting.

Distribution of binary data and the corresponding values of target variable.

warnings.simplefilter(action='ignore')

var = [col for col in train_copy.columns if '_bin' in col]

i = 0

s_bin = train_copy.sample(frac=0.1)

t1 = s_bin.loc[s_bin['target'] != 0]

t0 = s_bin.loc[s_bin['target'] == 0]

sns.set_style('whitegrid')

plt.figure()

fig, ax = plt.subplots(figsize=(15,20))

for feature in var:

i += 1

plt.subplot(4,3,i)

sns.kdeplot(t1[feature], bw=0.5, label="target = 1")

sns.kdeplot(t0[feature], bw=0.5, label="target = 0")

plt.legend(loc='best')

plt.ylabel('Density plot', fontsize=12)

plt.xlabel(feature, fontsize=12)

locs, labels = plt.xticks()

plt.tick_params(axis='both', which='major', labelsize=12)

plt.savefig('./plots/binary-features.png', dpi=fig.dpi)

plt.show()

<Figure size 432x288 with 0 Axes>

As the categorical variables are already numerical, there is no need to apply LabelEncoding.

Reference:

Raschka, S., & Mirjalili, V. (2019). Python Machine Learning. Zaltbommel, Netherlands: Van Haren Publishing.

# Feature scaling

numerical_features = meta[(meta.level == 'numerical')].index

features_n = numerical_features.to_list()

training_normalized = train_df.copy()

features = training_normalized[features_n]

scaler = StandardScaler().fit(features.values)

features = scaler.transform(features.values)

training_normalized[features_n] = features

training_data = training_normalized.copy()

lgb_params_f = {

'is_unbalance': True, # because training data is extremely unbalanced

'objective': 'binary',

'boosting_type': 'dart',

'learning_rate': 0.01,

'n_estimators': 500,

'n_jobs': 2, # number of parallel threads

'importance_type': 'gain'

}

features_classifier = lgb.LGBMClassifier()

features_classifier.set_params(**lgb_params_f)

y = training_data.target

X = training_data.drop(['target'], inplace=False, axis=1)

X, X_test, y, y_test = train_test_split(X, y, test_size = 0.2)

kf = StratifiedKFold(n_splits=5, shuffle=True, random_state=2021)

predicts = []

for train_index, test_index in kf.split(X, y):

print('-'*40)

X_train, X_val = X.iloc[train_index], X.iloc[test_index]

y_train, y_val = y.iloc[train_index], y.iloc[test_index]

features_classifier.fit(X_train, y_train, eval_set=[(X_val, y_val)], verbose=250, early_stopping_rounds=50)

#predicts.append(features_classifier.predict(X_test))

# saving the model

joblib_file = "./files/LightGBM_feature_importances.pkl"

joblib.dump(features_classifier, joblib_file)

try:

with open("./files/LightGBM_feature_importances.pkl") as f:

features_classifier = joblib.load(f.name)

X = train_df.drop(['target'], inplace=False, axis=1)

except IOError:

print("File not accessible")

#Plotting features importance

feature_imp = pd.DataFrame(sorted(zip(features_classifier.feature_importances_,X.columns)), columns=['Value','Feature'])

scaler_ft = MinMaxScaler()

feature_imp['Value'] = scaler_ft.fit_transform(feature_imp['Value'].values.reshape(-1,1))

fig = plt.figure(figsize=(15, 12))

sns.barplot(x="Value", y="Feature", data=feature_imp.sort_values(by="Value", ascending=False))

plt.title('LightGBM Features Importance by avg over folds')

plt.savefig('./plots/lgbm_importances.png', dpi=fig.dpi)

locs, labels = plt.xticks()

plt.tick_params(axis='both', which='major', labelsize=12)

plt.show()

Now that we have the Feature Importance, let's join the train and test data in order to perform transformation on both.

all_data = pd.concat([train_df, test_df], ignore_index=True)

all_data = all_data.drop('target', axis=1) # Remove target value

drop_features = ['ps_car_02_cat', 'ps_ind_14','ps_ind_10_bin',

'ps_ind_11_bin','ps_ind_12_bin','ps_ind_13_bin',

'ps_car_08_cat','ps_car_10_cat', 'ps_ind_18_bin', 'ps_car_09_cat', 'ps_car_05_cat']

all_data_remaining = all_data.drop(drop_features, axis=1)

print('Number of features before selection: {}'.format(all_data.shape[1]))

print('Number of features after selection: {}'.format(all_data_remaining.shape[1]))

Number of features before selection: 37 Number of features after selection: 26

all_data_feat_sel = all_data_remaining.copy()

The study of missing data was formalized by Donald Rubin with the concept of missing mechanism in which missing-data indicators are random variables and assigned a distribution. Missing data mechanism describes the underlying mechanism that generates missing data.

It is important to consider missing data mechanism when deciding how to deal with missing data. Because this is unknown, I will consider the missing data as part of the dataset (as a category) and just create a new feature adding the total number of missing data.

Rubin, D. B. (1975). INFERENCE AND MISSING DATA. ETS Research Bulletin Series, 1975(1), i–19. https://doi.org/10.1002/j.2333-8504.1975.tb01053.x

feature_names = all_data_feat_sel.columns.tolist()

num_features = [c for c in feature_names if '_cat' not in c]

all_data_feat_sel['missing'] = (all_data_feat_sel==-1).sum(axis=1).astype(float)

num_features.append('missing')

features_n = [col for col in all_data_feat_sel.columns if ('_cat' not in col and '_bin' not in col)]

all_data_n = all_data_feat_sel.copy()

features = all_data_n[features_n]

# using default

scaler = StandardScaler().fit(features.values)

features = scaler.transform(features.values)

all_data_n[features_n] = features

all_data_enc = all_data_n.copy()

categoricals_features = [col for col in all_data_feat_sel.columns if '_cat' in col]

print('Before dummification we have {} variables in train'.format(all_data_enc.shape[1]))

all_data_enc = pd.get_dummies(all_data_enc, columns=categoricals_features, drop_first=True)

print('After dummification we have {} variables in train'.format(all_data_enc.shape[1]))

Before dummification we have 27 variables in train After dummification we have 176 variables in train

num_train = train_df.shape[0] # Number of train data

final_data = all_data_enc.copy()

# Divide train data and test data

X = np.asarray(final_data[:num_train])

X_test = np.asarray(final_data[num_train:])

y = np.asarray(train_df['target'])

# Splitting the train to use 20% later on evaluation

X, X_eval, y, y_eval = train_test_split(X, y, test_size = 0.2)

def gini(actual, pred):

assert (len(actual) == len(pred))

all = np.asarray(np.c_[actual, pred, np.arange(len(actual))], dtype=np.float)

all = all[np.lexsort((all[:, 2], -1 * all[:, 1]))]

totalLosses = all[:, 0].sum()

giniSum = all[:, 0].cumsum().sum() / totalLosses

giniSum -= (len(actual) + 1) / 2.

return giniSum / len(actual)

def gini_normalized(actual, pred):

return gini(actual, pred) / gini(actual, actual)

lgb_params = {

'objective': 'binary',

'is_unbalance': True, # As we have a severe imbalanced class

'metric': 'auc',

'n_estimators': 500,

'n_jobs': 2,

'learning_rate': 0.01,

'num_leaves': 30

}

lgb_c = lgb.LGBMClassifier()

lgb_c.set_params(**lgb_params)

LGBMClassifier(is_unbalance=True, learning_rate=0.01, metric='auc',

n_estimators=500, n_jobs=2, num_leaves=30, objective='binary')

NOTE

Sets the weights of the dominated label to 1, and the weights of the dominant labels to the ratio of count of dominant/dominated.

K-fold cross-validation reports on the performance of a model on several (k) samples from your training set. This provides a less biased evaluation of the model. However, K-fold cross-validation is more computationally expensive than slicing your data into three parts. It re-fits the model and tests it k-times, for each iteration, as opposed to one time.

It can be beneficial for many reasons, for example, when your data set is not large enough to slice into three representative parts, cross-validation can help with that. Preventing overfitting to your test data without further reducing the size of your training data set.

%%time

preds_proba_lgb = np.zeros([X.shape[0],2])

preds_lgb = np.zeros(X.shape[0])

folds = StratifiedKFold(n_splits=5, shuffle=True, random_state=2021)

for n_fold, (train_index, test_index) in enumerate(folds.split(X, y)):

print('#'*40, f'Fold {n_fold+1} out of {folds.n_splits}', '#'*40)

X_train, y_train = X[train_index], y[train_index] # Train data

X_val, y_val = X[test_index], y[test_index] # Valid data

lgb_c.fit(X_train, y_train, eval_set=[(X_train, y_train), (X_val, y_val)],

verbose=250, early_stopping_rounds=50)

preds_proba_lgb[test_index] += lgb_c.predict_proba(X_val, raw_score=False)

preds_lgb[test_index] += lgb_c.predict(X_val, raw_score=False)

# Normalized Gini coefficient for prediction probabilities

gini_score = gini_normalized(y_val, preds_proba_lgb[test_index][:, 1])

print(f'Fold {n_fold+1} gini score: {gini_score}\n')

######################################## Fold 1 out of 5 ######################################## Training until validation scores don't improve for 50 rounds [250] training's auc: 0.671216 valid_1's auc: 0.6393 [500] training's auc: 0.688003 valid_1's auc: 0.641501 Did not meet early stopping. Best iteration is: [500] training's auc: 0.688003 valid_1's auc: 0.641501 Fold 1 gini score: 0.2830025558645673 ######################################## Fold 2 out of 5 ######################################## Training until validation scores don't improve for 50 rounds [250] training's auc: 0.672502 valid_1's auc: 0.63852 Early stopping, best iteration is: [308] training's auc: 0.676627 valid_1's auc: 0.639076 Fold 2 gini score: 0.2781511995670359 ######################################## Fold 3 out of 5 ######################################## Training until validation scores don't improve for 50 rounds [250] training's auc: 0.673034 valid_1's auc: 0.633694 Early stopping, best iteration is: [439] training's auc: 0.685421 valid_1's auc: 0.63508 Fold 3 gini score: 0.27015905173357696 ######################################## Fold 4 out of 5 ######################################## Training until validation scores don't improve for 50 rounds [250] training's auc: 0.670961 valid_1's auc: 0.640073 [500] training's auc: 0.687681 valid_1's auc: 0.641387 Did not meet early stopping. Best iteration is: [500] training's auc: 0.687681 valid_1's auc: 0.641387 Fold 4 gini score: 0.28277453019955767 ######################################## Fold 5 out of 5 ######################################## Training until validation scores don't improve for 50 rounds [250] training's auc: 0.672749 valid_1's auc: 0.636549 Early stopping, best iteration is: [445] training's auc: 0.686193 valid_1's auc: 0.637441 Fold 5 gini score: 0.27488291671262755 CPU times: user 6min 38s, sys: 4.67 s, total: 6min 43s Wall time: 3min 38s

LightGBM total: 6min 43s

# Save LightGBM model to file in the current working directory

joblib_file = "./files/lightgbm/LightGBM_Model.pkl"

joblib.dump(lgb_c, joblib_file)

with open('./files/lightgbm/evals_result.json', 'w') as fp:

json.dump(lgb_c.evals_result_, fp, sort_keys=True, indent=4)

np.savetxt('./files/lightgbm/preds_lgb.csv', preds_lgb, fmt = '%i')

np.savetxt('./files/lightgbm/preds_prob_lgb.csv', preds_proba_lgb, fmt = '%s', delimiter=",")

params_xgb = {

'objective': 'binary:logistic',

'learning_rate': 0.01,

'n_estimators': 500,

#'missing': -1,

'n_jobs': 2,

'random_state': 1986

}

xgb_model = xgb.XGBClassifier(**params_xgb)

%%time

preds_proba_xgb = np.zeros([X.shape[0],2])

preds_xgb = np.zeros(X.shape[0])

folds = StratifiedKFold(n_splits=5, shuffle=True, random_state=2021)

for n_fold, (train_index, test_index) in enumerate(folds.split(X, y)):

print('#'*40, f'Fold {n_fold+1} out of {folds.n_splits}', '#'*40)

X_train, y_train = X[train_index], y[train_index] # Train data

X_val, y_val = X[test_index], y[test_index] # Valid data

xgb_model.fit(X_train, y_train, eval_set=[(X_train, y_train), (X_val, y_val)],

eval_metric='auc', early_stopping_rounds=50, verbose = False)

preds_proba_xgb[test_index] += xgb_model.predict_proba(X_val)

preds_xgb[test_index] += xgb_model.predict(X_val)

# Normalized Gini coefficient for prediction probabilities

gini_score = gini_normalized(y_val, preds_proba_xgb[test_index][:, 1])

print(f'Fold {n_fold+1} gini score: {gini_score}\n')

XGBoost total: 3h 34min 42s

# Save XGBoost model to file in the current working directory

joblib_file = "./files/xgb/XGBoost_Model.pkl"

joblib.dump(xgb_model, joblib_file)

['./files/xgb/XGBoost_Model.pkl']

with open('./files/xgb/evals_result.json', 'w') as fp:

json.dump(xgb_model.evals_result_, fp, sort_keys=True, indent=4)

np.savetxt('./files/xgb/preds_xgb.csv', preds_xgb, fmt = '%i')

np.savetxt('./files/xgb/preds_prob_xgb.csv', preds_proba_xgb, fmt = '%s', delimiter=",")

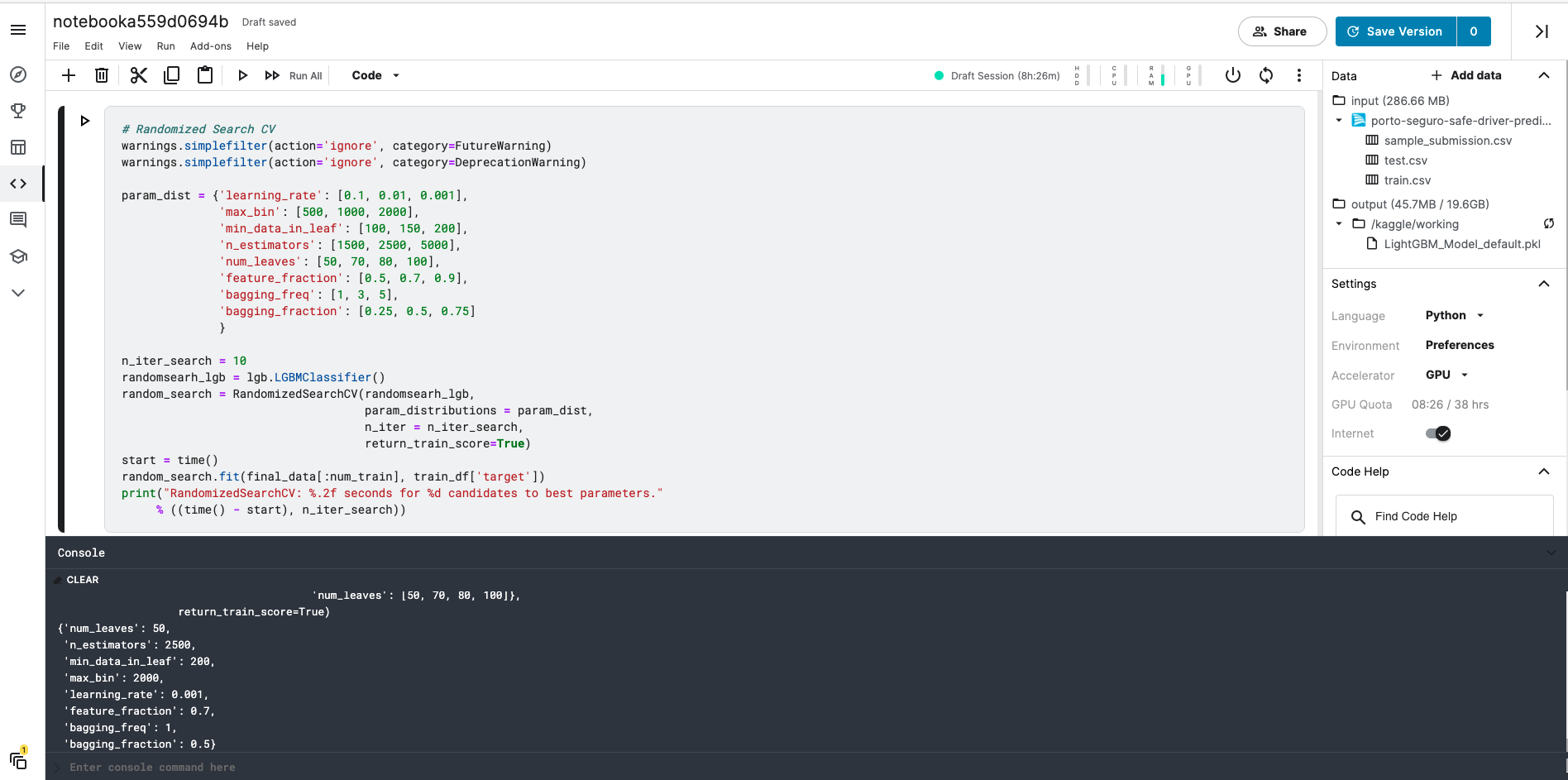

Random Search for Hyper-Parameter Optimization

https://lightgbm.readthedocs.io/en/latest/Parameters-Tuning.html

# Randomized Search CV

warnings.simplefilter(action='ignore', category=FutureWarning)

warnings.simplefilter(action='ignore', category=DeprecationWarning)

param_dist = {'learning_rate': [0.1, 0.01, 0.001],

'max_bin': [500, 1000, 2000],

'min_data_in_leaf': [500, 1000, 1500],

'n_estimators': [500, 1500, 2000],

'num_leaves': [10, 30, 50, 100],

'bagging_freq': [1, 3, 5],

'bagging_fraction': [0.25, 0.5, 0.75]

}

n_iter_search = 10

randomsearh_lgb = lgb.LGBMClassifier()

random_search = RandomizedSearchCV(randomsearh_lgb,

param_distributions = param_dist,

n_iter = n_iter_search,

return_train_score=True)

start = time()

random_search.fit(final_data[:num_train], train_df['target'])

print("RandomizedSearchCV: %.2f seconds for %d candidates to best parameters."

% ((time() - start), n_iter_search))

NOTE: Due to computing resources limitations I did not perform RandomizedSearchCV locally

Parameters Tuning was performed on Kaggle and yield the output below:

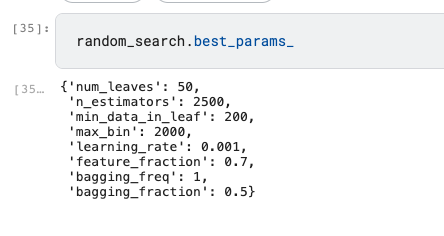

random_search.best_params_

lgb_params_tuned = {

'objective': 'binary',

'is_unbalance': True, # As we have a severe imbalanced class

'metric': 'auc',

'n_estimators': 2500,

'n_jobs': 2,

'num_leaves': 50,

'max_bin': 2000,

'learning_rate': 0.001,

'min_data_in_leaf': 200,

'feature_fraction': 0.7,

'bagging_freq': 1,

'bagging_fraction': 0.5

}

lgb_tuned = lgb.LGBMClassifier()

lgb_tuned.set_params(**lgb_params_tuned)

LGBMClassifier(bagging_fraction=0.5, bagging_freq=1, feature_fraction=0.7,

is_unbalance=True, learning_rate=0.001, max_bin=2000,

metric='auc', min_data_in_leaf=200, n_estimators=2500, n_jobs=2,

num_leaves=50, objective='binary')

%%time

preds_proba_lgb_tuned = np.zeros([X.shape[0],2])

preds_lgb_tuned = np.zeros(X.shape[0])

folds = StratifiedKFold(n_splits=5, shuffle=True, random_state=2021)

for n_fold, (train_index, test_index) in enumerate(folds.split(X, y)):

print('#'*40, f'Fold {n_fold+1} out of {folds.n_splits}', '#'*40)

X_train, y_train = X[train_index], y[train_index] # Train data

X_val, y_val = X[test_index], y[test_index] # Valid data

lgb_tuned.fit(X_train, y_train, eval_set=[(X_train, y_train), (X_val, y_val)],

verbose=1250, early_stopping_rounds=200)

preds_proba_lgb_tuned[test_index] += lgb_tuned.predict_proba(X_val)

preds_lgb_tuned[test_index] += lgb_tuned.predict(X_val)

# Normalized Gini coefficient for prediction probabilities

gini_score = gini_normalized(y_val, preds_proba_lgb_tuned[test_index][:, 1])

print(f'Fold {n_fold+1} gini score: {gini_score}\n')

######################################## Fold 1 out of 5 ######################################## Training until validation scores don't improve for 200 rounds [1250] training's auc: 0.679549 valid_1's auc: 0.640271 [2500] training's auc: 0.690902 valid_1's auc: 0.642823 Did not meet early stopping. Best iteration is: [2500] training's auc: 0.690902 valid_1's auc: 0.642823 Fold 1 gini score: 0.2856459142142984 ######################################## Fold 2 out of 5 ######################################## [LightGBM] [Warning] bagging_freq is set=1, subsample_freq=0 will be ignored. Current value: bagging_freq=1 [LightGBM] [Warning] min_data_in_leaf is set=200, min_child_samples=20 will be ignored. Current value: min_data_in_leaf=200 [LightGBM] [Warning] feature_fraction is set=0.7, colsample_bytree=1.0 will be ignored. Current value: feature_fraction=0.7 [LightGBM] [Warning] bagging_fraction is set=0.5, subsample=1.0 will be ignored. Current value: bagging_fraction=0.5 Training until validation scores don't improve for 200 rounds [1250] training's auc: 0.680844 valid_1's auc: 0.639883 [2500] training's auc: 0.692403 valid_1's auc: 0.640877 Did not meet early stopping. Best iteration is: [2500] training's auc: 0.692403 valid_1's auc: 0.640877 Fold 2 gini score: 0.2817546620283616 ######################################## Fold 3 out of 5 ######################################## [LightGBM] [Warning] bagging_freq is set=1, subsample_freq=0 will be ignored. Current value: bagging_freq=1 [LightGBM] [Warning] min_data_in_leaf is set=200, min_child_samples=20 will be ignored. Current value: min_data_in_leaf=200 [LightGBM] [Warning] feature_fraction is set=0.7, colsample_bytree=1.0 will be ignored. Current value: feature_fraction=0.7 [LightGBM] [Warning] bagging_fraction is set=0.5, subsample=1.0 will be ignored. Current value: bagging_fraction=0.5 Training until validation scores don't improve for 200 rounds [1250] training's auc: 0.681126 valid_1's auc: 0.634423 [2500] training's auc: 0.692382 valid_1's auc: 0.636081 Did not meet early stopping. Best iteration is: [2500] training's auc: 0.692382 valid_1's auc: 0.636081 Fold 3 gini score: 0.27216282452754054 ######################################## Fold 4 out of 5 ######################################## [LightGBM] [Warning] bagging_freq is set=1, subsample_freq=0 will be ignored. Current value: bagging_freq=1 [LightGBM] [Warning] min_data_in_leaf is set=200, min_child_samples=20 will be ignored. Current value: min_data_in_leaf=200 [LightGBM] [Warning] feature_fraction is set=0.7, colsample_bytree=1.0 will be ignored. Current value: feature_fraction=0.7 [LightGBM] [Warning] bagging_fraction is set=0.5, subsample=1.0 will be ignored. Current value: bagging_fraction=0.5 Training until validation scores don't improve for 200 rounds [1250] training's auc: 0.680107 valid_1's auc: 0.642059 [2500] training's auc: 0.691654 valid_1's auc: 0.643793 Did not meet early stopping. Best iteration is: [2500] training's auc: 0.691654 valid_1's auc: 0.643793 Fold 4 gini score: 0.2875865568406136 ######################################## Fold 5 out of 5 ######################################## [LightGBM] [Warning] bagging_freq is set=1, subsample_freq=0 will be ignored. Current value: bagging_freq=1 [LightGBM] [Warning] min_data_in_leaf is set=200, min_child_samples=20 will be ignored. Current value: min_data_in_leaf=200 [LightGBM] [Warning] feature_fraction is set=0.7, colsample_bytree=1.0 will be ignored. Current value: feature_fraction=0.7 [LightGBM] [Warning] bagging_fraction is set=0.5, subsample=1.0 will be ignored. Current value: bagging_fraction=0.5 Training until validation scores don't improve for 200 rounds [1250] training's auc: 0.681242 valid_1's auc: 0.636543 [2500] training's auc: 0.692865 valid_1's auc: 0.638097 Did not meet early stopping. Best iteration is: [2500] training's auc: 0.692865 valid_1's auc: 0.638097 Fold 5 gini score: 0.2761939916808852 CPU times: user 1h 5min 35s, sys: 27.8 s, total: 1h 6min 3s Wall time: 33min 35s

LightGBM Tuned total: 1h 6min 3s

# Save LightGBM model to file in the current working directory

joblib_file = "./files/lightgbm/LightGBM_tuned.pkl"

joblib.dump(lgb_tuned, joblib_file)

['./files/lightgbm/LightGBM_tuned.pkl']

with open('./files/lightgbm/evals_result_tuned.json', 'w') as fp:

json.dump(lgb_tuned.evals_result_, fp, sort_keys=True, indent=4)

np.savetxt('./files/lightgbm/preds_lgb_tuned.csv', preds_lgb_tuned, fmt = '%i')

np.savetxt('./files/lightgbm/preds_prob_lgb_tuned.csv', preds_proba_lgb_tuned, fmt = '%s', delimiter=",")

The Gini index or Gini coefficient is a statistical measure of distribution that was developed by the Italian statistician Corrado Gini in 1912. It is used as a gauge of economic inequality, measuring income distribution among a population.

The Gini coefficient is equal to the area below the line of perfect equality (0.5 by definition) minus the area below the Lorenz curve, divided by the area below the line of perfect equality. In other words, it is double the area between the Lorenz curve and the line of perfect equality.

Gini is a vital metric for insurers because the main concern focuses on segregating high and low risks rather than predicting losses. The reason is that this information is used to price insurance risks and charging customers on their predicted loss is not accountable for expenses and profit.

Since this task is classification, AUC was used as a metric because it's equivalent to using Gini since:

$$ Gini = 2 * AUC - 1 $$In order to compute gini coefficient we should apply two integrals with the cumulative proportion of positive class

$$A=\int_{0}^{1}F(x)dx\approx \sum_{i=1}^{n}F_{i}(x)\times \frac{1}{n}$$$$B=\int_{0}^{1}x \; dx\approx \sum_{i=1}^{n}\frac{i}{n} \times \frac{1}{n}= \frac{1}{n^{2}}\times \frac{n\times (n+1)}{2}\approx 0.5$$$$Gini\, coeff= A-B=\frac{1}{n}\left (\sum_{i=1}^{n}F_{i}(x) -\frac{n+1}{2} \right)$$Because both classes are important due to the segregating aspect mentioned on the Gini coefficient, the evaluation metric chosen will be AUC.

lightgbm_model = joblib.load('./files/lightgbm/LightGBM_Model.pkl')

preds_lgb = np.fromstring(loadtxt('./files/lightgbm/preds_lgb.csv'))

preds_prob_lgb = np.loadtxt('./files/lightgbm/preds_prob_lgb.csv', delimiter=',')

lightgbm_eval_probs = lightgbm_model.predict_proba(X_eval)

lightgbm_eval_probs = lightgbm_eval_probs[:, 1]

roc_auc_lightgbm = roc_auc_score(y_eval, lightgbm_eval_probs)

print('LightGBM ROC AUC %.3f' % roc_auc_lightgbm)

LightGBM ROC AUC 0.666

# fpr = FalsePositiveRate

# tpr = TruePositiveRate

# calculate roc curves

fpr_lgbm, tpr_lgbm, thresholds_lgbm = roc_curve(y_eval, lightgbm_eval_probs)

# get the best threshold

J_lgbm = tpr_lgbm - fpr_lgbm # Youden's index

ix_lgbm = argmax(J_lgbm)

best_thresh_lgbm = thresholds_lgbm[ix_lgbm]

print('Best Threshold for LightGBM Model= %f' % (best_thresh_lgbm))

Best Threshold for LightGBM Model= 0.486313

lgbm_gini= gini(y_eval, lightgbm_eval_probs)

lgbm_gini_max = gini(y_eval, y_eval)

lgbm_ngini= gini_normalized(y_eval, lightgbm_eval_probs)

print('Gini: %.3f \nMax. Gini: %.3f \nNormalized Gini: %.3f' % (lgbm_gini, lgbm_gini_max, lgbm_ngini))

Gini: 0.160 Max. Gini: 0.482 Normalized Gini: 0.332

# Sort the actual values by the predictions

data_lgb = np.asarray(np.c_[y_eval, lightgbm_eval_probs,np.arange(len(y_eval))])

sorted_actual_lgb= data_lgb[np.lexsort((data_lgb[:,2],-1 * data_lgb[:, 1]))][:,0]

# Sum up the actual values

cumulative_actual_lgb = np.cumsum(sorted_actual_lgb)

cumulative_index_lgb = np.arange(1, len(cumulative_actual_lgb)+1)

cumulative_actual_shares_lgb = cumulative_actual_lgb / sum(y_eval)

cumulative_index_shares_lgb = cumulative_index_lgb / len(lightgbm_eval_probs)

# Add (0, 0) to the plot

x_values_lgb = [0] + list(cumulative_index_shares_lgb)

y_values_lgb = [0] + list(cumulative_actual_shares_lgb)

# Display the 45° line stacked on top of the y values

diagonal_lgb = [x - y for (x, y) in zip(x_values_lgb, y_values_lgb)]

plt.stackplot(x_values_lgb, y_values_lgb, diagonal_lgb, colors=['tab:blue', 'tab:orange'])

plt.legend(['_nolegend_','Gini Coefficient'], loc=2)

plt.xlabel('Cumulative Share of Predictions')

plt.ylabel('Cumulative Share of Actual Values')

plt.title('LightGBM | Gini = %.3f'%lgbm_gini)

plt.show()

xgb_model = joblib.load('./files/xgb/XGBoost_Model.pkl')

preds_xgb = np.fromstring(loadtxt('./files/xgb/preds_xgb.csv'))

preds_prob_xgb = np.loadtxt('./files/xgb/preds_prob_xgb.csv', delimiter=',')

xgb_eval_probs = xgb_model.predict_proba(X_eval)

xgb_eval_probs = xgb_eval_probs[:, 1]

# calculate roc curves

fpr_xgb, tpr_xgb, thresholds_xgb = roc_curve(y_eval, xgb_eval_probs)

# get the best threshold

J_xgb = tpr_xgb - fpr_xgb # Youden's index

ix_xgb = argmax(J_xgb)

best_thresh_xgb = thresholds_xgb[ix_xgb]

print('Best Threshold for XGBoost Model= %f' % (best_thresh_xgb))

Best Threshold for XGBoost Model= 0.040153

roc_auc_xgb = roc_auc_score(y_eval, xgb_eval_probs)

print('XGBoost ROC AUC %.3f' % roc_auc_xgb)

XGBoost ROC AUC 0.666

xgb_gini= gini(y_eval, xgb_eval_probs)

xgb_gini_max = gini(y_eval, y_eval)

xgb_ngini= gini_normalized(y_eval, xgb_eval_probs)

print('Gini: %.3f \nMax. Gini: %.3f \nNormalized Gini: %.3f' % (xgb_gini, xgb_gini_max, xgb_ngini))

Gini: 0.160 Max. Gini: 0.482 Normalized Gini: 0.332

# Sort the actual values by the predictions

data_xgb = np.asarray(np.c_[y_eval, xgb_eval_probs,np.arange(len(y_eval))])

sorted_actual_xgb= data_lgb[np.lexsort((data_xgb[:,2],-1 * data_xgb[:, 1]))][:,0]

# Sum up the actual values

cumulative_actual_xgb = np.cumsum(sorted_actual_xgb)

cumulative_index_xgb = np.arange(1, len(cumulative_actual_xgb)+1)

cumulative_actual_shares_xgb = cumulative_actual_xgb / sum(y_eval)

cumulative_index_shares_xgb = cumulative_index_xgb / len(xgb_eval_probs)

# Add (0, 0) to the plot

x_values_xgb = [0] + list(cumulative_index_shares_xgb)

y_values_xgb = [0] + list(cumulative_actual_shares_xgb)

# Display the 45° line stacked on top of the y values

diagonal_xgb = [x - y for (x, y) in zip(x_values_xgb, y_values_xgb)]

plt.stackplot(x_values_xgb, y_values_xgb, diagonal_xgb, colors=['tab:blue', 'tab:orange'])

plt.legend(['_nolegend_','Gini Coefficient'], loc=2)

plt.xlabel('Cumulative Share of Predictions')

plt.ylabel('Cumulative Share of Actual Values')

plt.title('XGBoost | Gini = %.3f'%xgb_gini)

plt.show()

lightgbm_tuned = joblib.load('./files/lightgbm/LightGBM_tuned.pkl')

preds_lgb_tuned = np.fromstring(loadtxt('./files/lightgbm/preds_lgb_tuned.csv'))

preds_prob_lgb_tuned = np.loadtxt('./files/lightgbm/preds_prob_lgb_tuned.csv', delimiter=',')

lightgbm_tuned_eval_probs = lightgbm_tuned.predict_proba(X_eval)

lightgbm_tuned_eval_probs = lightgbm_tuned_eval_probs[:, 1]

roc_auc_lightgbm_tuned = roc_auc_score(y_eval, lightgbm_tuned_eval_probs)

print('LightGBM Tuned ROC AUC %.3f' % roc_auc_lightgbm_tuned)

LightGBM Tuned ROC AUC 0.676

# calculate roc curves

fpr_lgbm_tuned, tpr_lgbm_tuned, thresholds_lgbm_tuned = roc_curve(y_eval, lightgbm_tuned_eval_probs)

# get the best threshold

J_lgbm_tuned = tpr_lgbm_tuned - fpr_lgbm_tuned # Youden's index

ix_lgbm_tuned = argmax(J_lgbm_tuned)

best_thresh_lgbm_tuned = thresholds_lgbm_tuned[ix_lgbm_tuned]

print('Best Threshold for LightGBM Tuned Model= %f' % (best_thresh_lgbm_tuned))

Best Threshold for LightGBM Tuned Model= 0.457183

lgbm_tuned_gini= gini(y_eval, lightgbm_tuned_eval_probs)

lgbm_tuned_gini_max = gini(y_eval, y_eval)

lgbm_tuned_ngini= gini_normalized(y_eval, lightgbm_tuned_eval_probs)

print('Gini: %.3f \nMax. Gini: %.3f \nNormalized Gini: %.3f' % (lgbm_tuned_gini,

lgbm_tuned_gini_max,

lgbm_tuned_ngini))

Gini: 0.170 Max. Gini: 0.482 Normalized Gini: 0.352

# Sort the actual values by the predictions

data_lgbm_tuned = np.asarray(np.c_[y_eval, lightgbm_tuned_eval_probs,np.arange(len(y_eval))])

sorted_actual_lgbm_tuned = data_lgbm_tuned[np.lexsort((data_lgbm_tuned[:,2],-1 * data_lgbm_tuned[:, 1]))][:,0]

# Sum up the actual values

cumulative_actual_lgbm_tuned = np.cumsum(sorted_actual_lgbm_tuned)

cumulative_index_lgbm_tuned = np.arange(1, len(cumulative_actual_lgbm_tuned)+1)

cumulative_actual_shares_lgbm_tuned = cumulative_actual_lgbm_tuned / sum(y_eval)

cumulative_index_shares_lgbm_tuned = cumulative_index_lgbm_tuned / len(lightgbm_tuned_eval_probs)

# Add (0, 0) to the plot

x_values_lgbm_tuned = [0] + list(cumulative_index_shares_lgbm_tuned)

y_values_lgbm_tuned = [0] + list(cumulative_actual_shares_lgbm_tuned)

# Display the 45° line stacked on top of the y values

diagonal_lgbm_tuned = [x - y for (x, y) in zip(x_values_lgbm_tuned, y_values_lgbm_tuned)]

plt.stackplot(x_values_lgbm_tuned, y_values_lgbm_tuned, diagonal_lgbm_tuned, colors=['tab:blue', 'tab:orange'])

plt.legend(['_nolegend_','Gini Coefficient'], loc=2)

plt.xlabel('Cumulative Share of Predictions')

plt.ylabel('Cumulative Share of Actual Values')

plt.title('LightGBM Tuned | Gini = %.3f'%lgbm_tuned_gini)

plt.show()

# plot the roc curve for the model

plt.plot([0,1], [0,1], linestyle='--')

plt.plot(fpr_lgbm, tpr_lgbm, label='LightGBM (AUC = %.2f)' % roc_auc_lightgbm)

plt.plot(fpr_lgbm_tuned, tpr_lgbm_tuned, label='LightGBM Tuned (AUC = %.2f)' % roc_auc_lightgbm_tuned)

plt.plot(fpr_xgb, tpr_xgb, label='XGBoost (AUC = %.2f)' % roc_auc_xgb)

# axis labels

plt.xlabel('False Positive Rate')

plt.ylabel('True Positive Rate')

plt.title('ROC Area Under Curve')

plt.legend()

# show the plot

plt.show()

All 3 models' performance (AUC) were very similar and using Random Search for Hyper-Parameter Optimization only increased 0.01 in AUC metric. One interesting point was about two models with the same score, LightGBM (first version) and XGBoost, but with almost 3,5 hours difference in training time.

| Model | Normalized Gini | AUC | Training time |

|---|---|---|---|

| LightGBM | 0.33 | 0.67 | 6min 43s |

| XGBoost | 0.33 | 0.67 | 3h 34min 42s |

| LightGBM Tuned | 0.35 | 0.68 | 1h 6min 3s |

# X_test is the test.csv provided with all transformations applied

test_preds_lgb = lightgbm_tuned.predict_proba(X_test)

test_preds_xgb = xgb_model.predict_proba(X_test)

# slicing to get the probability for the positive class only

test_preds_lgb = test_preds_lgb[:,1:]

test_preds_xgb = test_preds_xgb[:,1:]

submission = pd.read_csv(path + 'sample_submission.csv', index_col='id')

submission['target'] = test_preds_lgb

submission.to_csv('./kaggle-submission/LightGBM.csv')

submission = pd.read_csv(path + 'sample_submission.csv', index_col='id')

submission['target'] = test_preds_xgb

submission.to_csv('./kaggle-submission/XGBoost.csv')

submission = pd.read_csv(path + 'sample_submission.csv', index_col='id')

ensemble_test_preds = test_preds_lgb * 0.6 + test_preds_xgb * 0.4

submission['target'] = ensemble_test_preds

submission.to_csv('./kaggle-submission/Ensemble.csv')

GitHub repository

GitHub repository

Author: Leandro Pessini